The true value of start-ups

Venture capital funds intermittently have to report the holding value of their portfolio to their limited partners (their investors).

Now a company may take 3-10 years after investment to be sold, listed or liquidated, and in the interim the stock is very illiquid.

So in order to value a whole venture portfolio the value of each start-up in the portfolio also has to be guessed at.

The usual approach is to take the value of the last round of funding as the last crystallised valuation point. It’s as good as it gets.

The issue of course is that VCs overpay for their stock and in return they get liquidation preference rights (the right to get their money out first and a double dip on their investment) as well as control/veto rights.

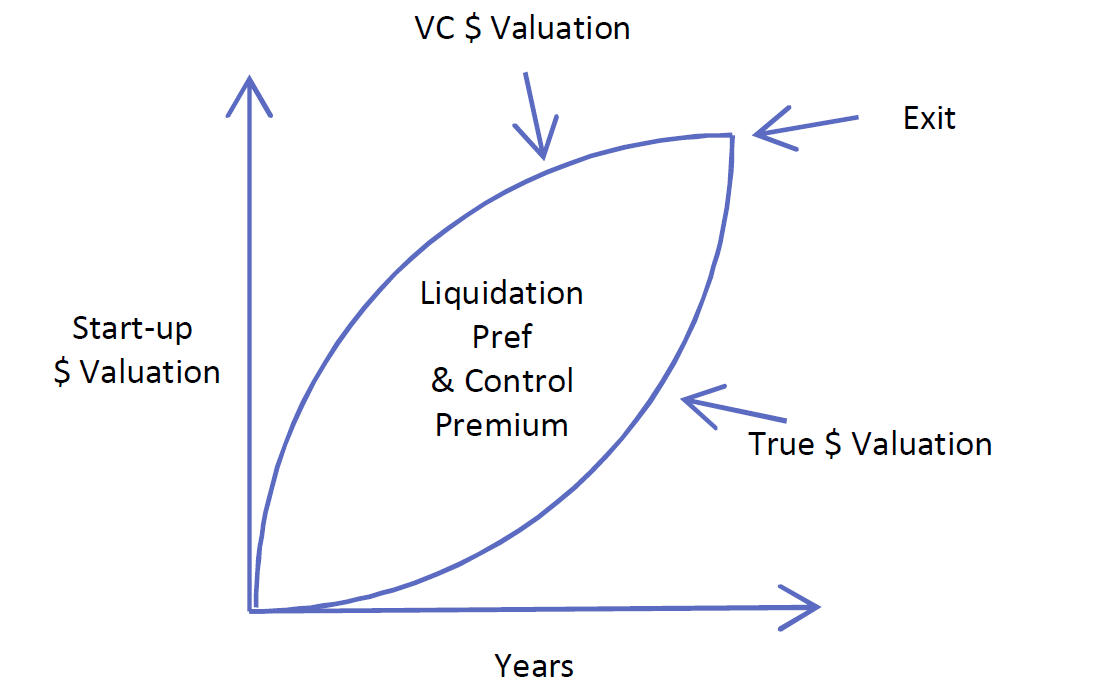

My personal view is that the true valuation of a start-up and that calculated by the last round post-money valuation is separated by a fair gap – as per the chart below.

A more accurate means to estimate the true value of the company at any moment is to subtract the total of all liquidation preferences from the last post-money valuation.

This approach is very simple for a VC to validate – I say to them; liquidate your portfolio today and I am sure your proceeds will be far closer to the common stock valuation (or less) than the full last round valuation, inclusive of a liquidation preference premium.

By taking into account the liquidation preference premium into your holding value you are inherently introducing a bias towards a successful outcome (the two lines meeting in the plot below) for all the companies in your portfolio. Which you know is not the case.